Time is money. That is perhaps one of the most shared and lived-by aphorisms in our everyday lives and work principles. This makes the prediction of success rates and forecast time and financial status for projects one of the most important and challenging aspects of project control.

Creating a baseline program with measurement tools to record project progress is utilized to manage the project time and cost updates. The main methods available for a project planner to adopt with the project baseline are the “time-phased budget” and “Cost Loaded Schedule”.

Whilst both of these methods can be adapted to update and monitor the project baseline, each has its advantages and disadvantages and value to the project management team.

First things first, what is the goal of schedule loading and budgeting?

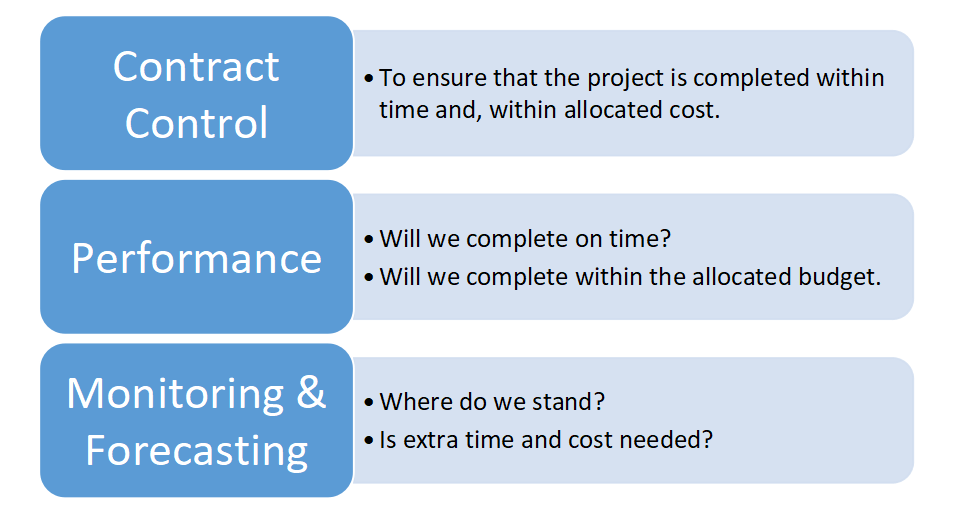

Planning and coordinating are crucial to the project’s success; therefore, planners are always concerned with the time and cost parameters for the project’s success. This can be easily illustrated by the following tags and questions, as shown below:

What is a Cost-Loaded Schedule?

A cost loaded uses planning software, commonly Primavera P6 or MS-Project, to create a baseline schedule with proper sequencing, logic, relationships, resources, and materials to achieve the project completion dates. The cost-loaded schedule is the output of the estimated/ planned costs “loaded” in the schedule.

Although there are several excel templates, macros, and third-party software that targets automating the estimation and cost-loading process, a large portion of the work done is manual and requires input and focus from the planner.

These challenges and efforts include:

- The actual creation of the schedule (scheduling) and creating the correct Work Breakdown Structure and activities. This is extremely important as the ultimate resources and loading will be done to the activities, therefore, they must be correctly described and up to the most realistic and smallest level possible. Otherwise, the result will be an unrealistic baseline schedule cost loading.

- Coordinating with other disciplines in activity loading and methodology. It is commonly used to monitor MEP activities by Man-Hours, whilst Civil/ Structural activities such as block work installation by quantity.

- The allocation of INDIRECT and other costs or fees. The main issue is; they have a weightage but cannot be confined to a certain resource-loaded activity. Most planners opt to add these costs under the level of effort activities linked with the project duration (start and finish).

It is also important to note that other items that arise after the project start and the creation of a baseline such as:

- Subcontract Agreements,

- Extensive variations and cost changes.

- Maintenance of dummy and level of effort activities to balance cost forecast and approved budget.

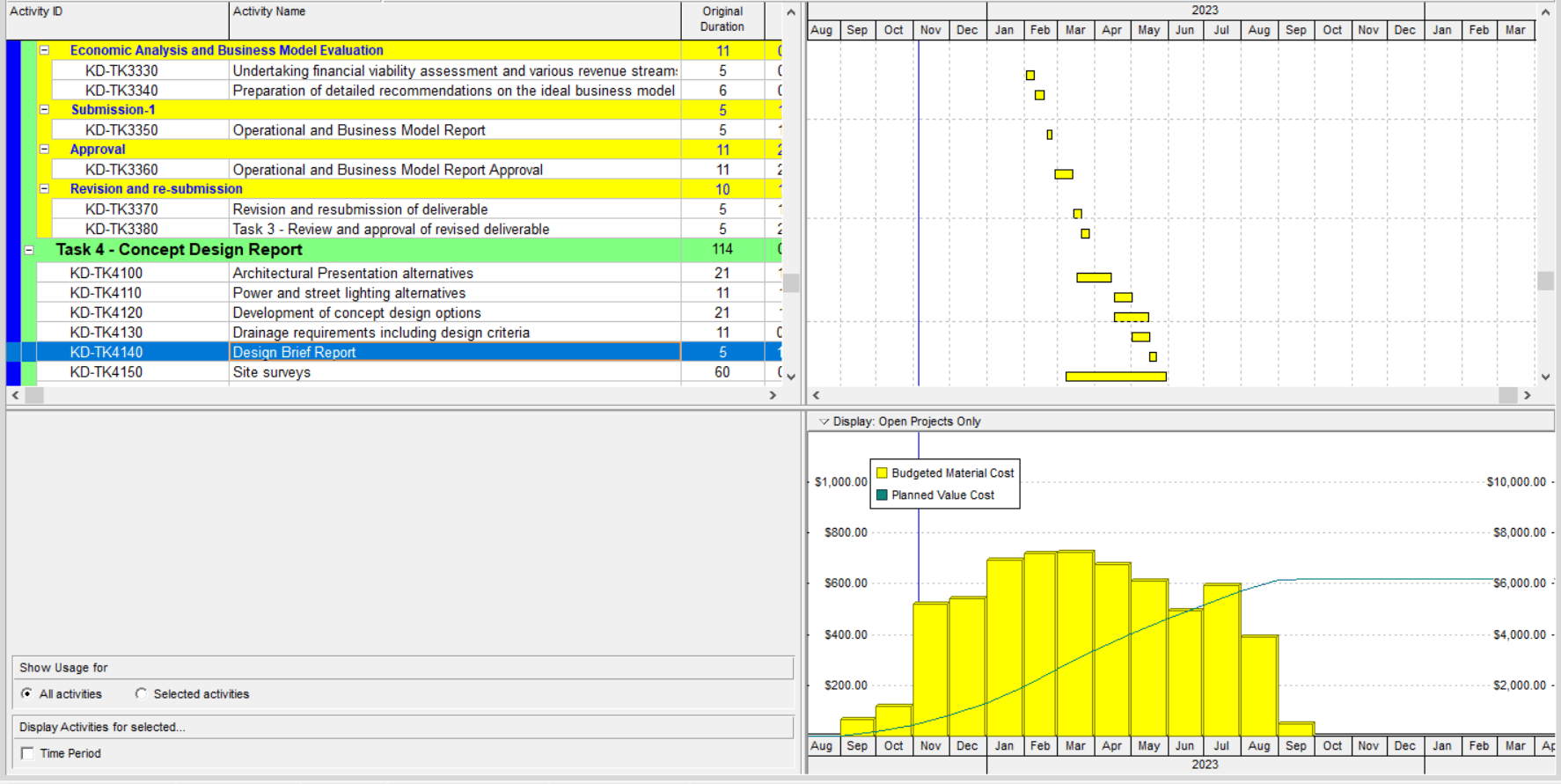

Below is an example of a Budgeted Total cost graph along with the project planned S-Curve after loading costs into the schedule:

TIP: Cost loading must be done in Parallel with scheduling to avoid repetitive work! This can be done by adding the know costs for a certain cycle of repetitive activities and then copy-pasting them to reflect the total scope and overall cost.

What is a Time-Phased Budget?

Time – phased budget concept is based on using a control account to link the schedule and estimated cost, unlike Cost loading, which does not depend on merging them. In layman’s terms, it demonstrates the planned spending of the allocated budget over time.

So, what is a control account?

A control account’s purpose is to integrate the project scope with the allocated time and budget at an organizational level. It is further explained in the 10S-90 Cost Accounting Terminology issued by the AACEI as “A management control point where earned value measurement takes place. It is the place where scope, schedule, and budget, are integrated at the organizational level responsible for the day-to-day management of a segment of the project”.

There are dedicated software such as ARES PRISM, but it is also noteworthy to point out that Primavera P6 does have a Cost Account Feature.

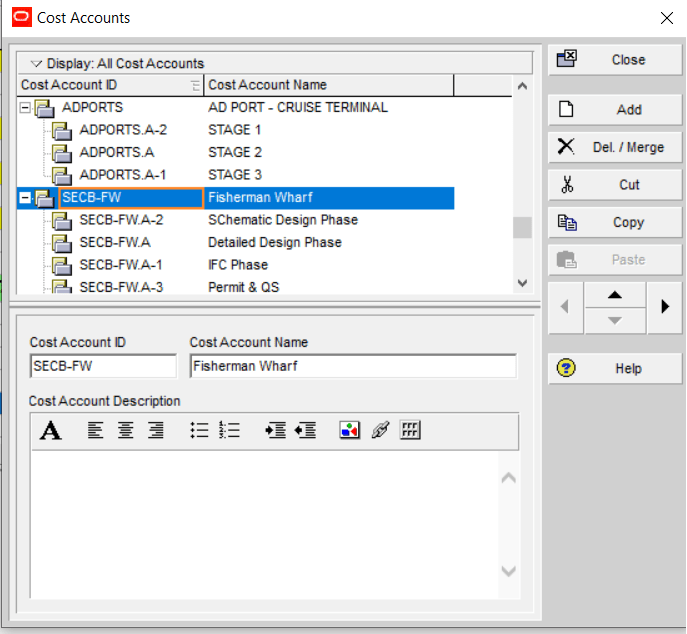

See the below example for a very high-level extract of Cost Accounts in Primavera P6:

The main difference between a Time-Phased Budget and Schedule Cost loading is that more than one activity can be assigned to a cost account. This is similar to a BOQ with several sub-items under the BOQ.

Since activities are assigned a cost account, the schedule duration and integrated cost can be used for generating S-curves and monitoring tools (In a similar way to the schedule loading).

Advantages and disadvantages:

The main advantages are:

- Time-Phased method does not depend on resource and quantity estimates, rates..etc, it directly uses the actual BOQ costs. Therefore, a lot of tedious work burden is reduced by the planner.

- Budget change can easily be reflected.

- Since less input is required, maintenance and generating forecasts are easier.

- Costs of Level of effort activities become easier.

The main disadvantages are:

- Not all planners are confident in working with Cost Accounts. More confusion arises when Activity Codes used for filtering and sorting are confused with Cost Accounts.

- From personal construction site experience, confusion arises in time-location activities and when resources required for an activity are compared to the Cost Account and curves/ forecasts generated. This is better explained by the following example:

Asphalt works for a bridge over a highway costs will most likely be under Pavement/ Asphalt Cost Account, but the actual activity will be performed on the structural elements/ scope of works whilst requiring Pavement resources.

Overall Comparison between the two methods:

| Description | Time Phased Budget | Cost-Loaded Schedule |

| Accuracy | Higher | Lower |

| Preparation/ Assigning time | Lower

(However, both require time to properly establish) |

Higher |

| Optimum Loading Strategy | During Scheduling | During scheduling |

| Maintenance Effort | Relatively Lower | Higher |

| Forecasting | More Accurate | Acceptable – Time Consuming |

| Sensitivity and Confidentiality | High | High |

| Earned Value Management | Acceptable | Acceptable |

| Cost – Activity Matching | Simpler | More Effort Required |

Extra Tips:

- It is recommended to prepare a properly loaded schedule and obtain approval on the project Baseline.

- Pre-project estimates and resource plans should always be stored and later used in comparison with the At-completion costs for informative lessons learned.

- The Project Baseline must be regularly updated and maintained with backup copies.

Summary

In Conclusion, both methods can be used for monitoring and earned value management. However, for large projects, it is recommended to implement both methods (IF POSSIBLE) for satisfying the construction site level requirements and the organizational level requirements.

During the project initiation phase and depending on the Contract type, the most suitable type should be decided by the planner and project management team. This is extremely important for Design – Build projects with fixed lump prices to avoid any issues in the monitoring process and in change requests.